Every rise in UK government bond yields seems to invite the same question. Is the market losing faith in Britain?

It is an understandable concern. Higher gilt yields raise the cost of government borrowing, affect mortgage pricing, and influence the returns available across portfolios. But the yield level on its own does not tell us whether the UK is in crisis. What matters is why yields are rising, whether the move is global or UK-specific, and whether investors are demanding a clear extra premium to lend to the British government.

For much of the past two decades, investors became used to unusually low interest rates. After the financial crisis, and again after Covid, cash and government bonds often offered little or no real return after inflation. That world felt comfortable in some ways. Borrowing was cheap, asset prices were supported, and governments could finance themselves with limited pain.

But money being too cheap for too long also has a cost. It can encourage poor decisions. Households, companies and governments all behave differently when debt feels almost free.

A simple way to think about this is the price of a ticket. If entry to a concert is free, more people will turn up, whether they really value the performance or not. If the ticket has a sensible price, people make a more deliberate decision. Interest rates work in a similar way. They are the price of money. When that price is zero, behaviour changes. When it is positive in real terms, capital has to be treated with more care.

This is why a gilt yield close to 5% is not automatically bad news. It clearly has consequences for public finances, and those consequences should not be dismissed. But it also means investors can once again earn a meaningful return from assets that are designed to act as portfolio stabilisers. That is healthier than a world in which investors are pushed into taking more risk simply because safer assets offer nothing.

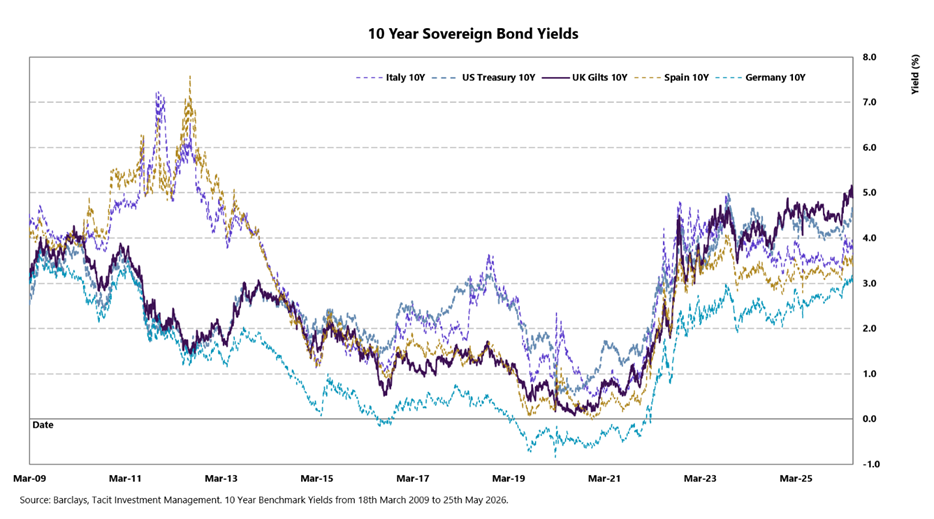

The chart below helps put this into context by comparing UK 10-year gilt yields with 10-year government bond yields in Italy, Spain, Germany and the US. The useful lesson is not that the UK has no problems. It plainly does. The point is that higher yields have been part of a wider global adjustment, not simply a British story.

The key distinction is between a general repricing of money and a specific loss of confidence in one borrower. If UK yields rise because inflation expectations, central bank policy and global bond yields are all moving higher, that is one type of challenge. If UK yields rise sharply while comparable markets remain stable, that would be a more serious signal.

That was the lesson of the eurozone sovereign debt crisis. Italian and Spanish yields did not merely rise with global markets, they climbed sharply relative to Germany, and investors were questioning country-specific credit and political risks.

The UK is not at that point. But nor should investors be complacent. Public finances are stretched, growth is modest, and inflation has been difficult to tame. These things matter because bond markets ultimately judge credibility, discipline and future cashflows. At Tacit, we think the sensible response is to watch the relative moves, not just the headline level. The UK has issues, but it is not alone. What matters is whether it becomes a genuine outlier, whether inflation continues to be brought under control, and whether investors are being paid sensibly for the risks they are taking.